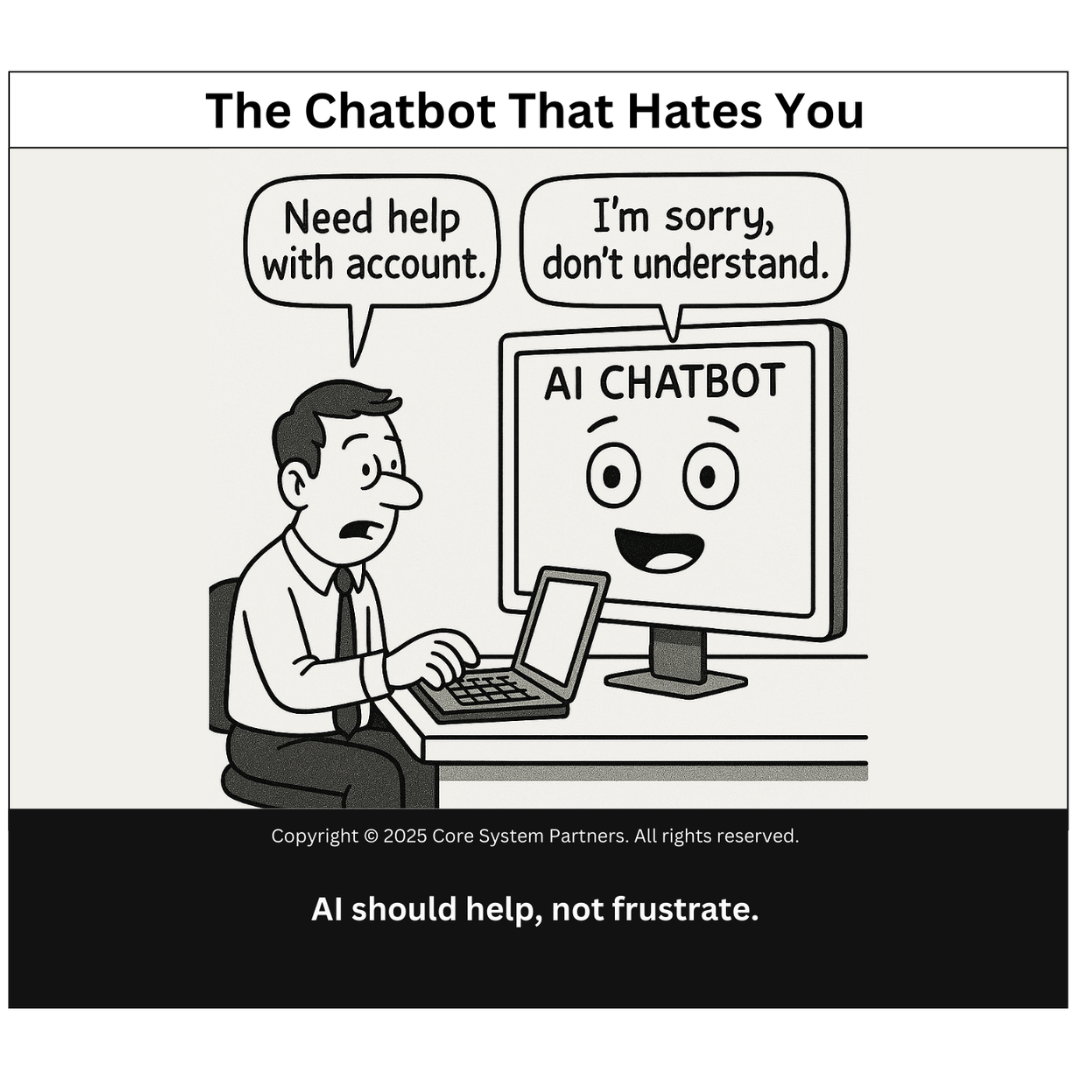

When AI chatbots fail to understand simple banking requests, frustration grows. AI should empower customers—not alienate them.

The 30-Step Login Process: Why Your Customers Are Giving Up

“I just wanted to check my balance…”

That line from the cartoon perfectly captures the problem. A user taps your banking app hoping for a two-second task—and is immediately dumped into a gauntlet of security checks.

Enter username.

Answer a security question.

Check your email.

Check your phone.

Resend the code.

Start over because your session expired.

It’s not just annoying. It’s a loyalty risk.

In a world built on immediacy, clunky login flows aren’t just bad UX—they’re a threat to your transformation goals. Customers expect banking to be as seamless as shopping, streaming, or ordering dinner. When it’s not, they don’t complain. They just leave.

The Quiet Killer of Digital Transformation

Too many banks spend millions on core modernization, only to wrap it in legacy logic. The engine might be new, but the access is still stuck in 2008.

We’ve seen it firsthand. One client upgraded to a state-of-the-art core, but kept their old authentication model. Result? Mobile login times ballooned to over a minute—and user satisfaction dropped like a rock.

The irony? The tech was solid. But the friction at the front door erased the benefits.

It’s like building a luxury hotel and locking the lobby behind a maze.

Security and Simplicity Aren’t Opposites

There’s a persistent myth that more steps mean more safety. But in reality, more steps often mean more frustration, more support calls, and more abandoned sessions.

And it doesn’t have to be that way.

Banks can—and should—embrace security models that blend protection with convenience:

- Risk-based authentication: Only escalate friction when behavior is suspicious.

- Biometric login: Fast, secure, and already built into every phone.

- Session intelligence: Keep users authenticated across trusted devices without repeating steps.

- Invisible checks: Device reputation, IP analysis, and behavioral biometrics behind the scenes.

If the goal is customer trust, making them jump through hoops isn’t the way to earn it.

Anecdote from the Field: When Login Blocks Growth

A regional credit union we worked with had a login flow that included:

- Username and password

- Two separate MFA prompts

- A CAPTCHA

- And a final session expiry warning

All before users even reached their dashboard.

The result? An 80% drop-off on the first login attempt. They had invested heavily in digital onboarding—but few customers made it far enough to experience it.

After retooling the flow with biometric fallback and context-aware authentication, their conversion doubled—and their support tickets halved.

It wasn’t magic. It was just a reminder: you can’t modernize the back end and ignore the front.

So What Does Frictionless Really Mean?

Let’s break it down. “Frictionless” doesn’t mean “lawless” or “insecure.” It means:

- Smart friction: Intervene only when needed. Trust your system to tell the difference.

- Predictive experience: Recognize safe behavior and reduce steps for returning users.

- Customer-first logic: Design flows for your average customer, not your worst-case scenario.

- Omnichannel simplicity: Ensure login flows are consistent, whether mobile, desktop, or in-branch.

Because today’s customer doesn’t separate “digital experience” from “banking experience.” It’s all the same to them.

5 Moves Toward Login Simplicity

If you’re serious about reducing friction without reducing safety, start here:

- Audit your entire login flow. Look for dead ends, repeated asks, and steps that add no real value.

- Introduce biometric login. Most customers already use Face ID or fingerprint tech elsewhere.

- Use step-up security. Only prompt for additional verification when behavior justifies it.

- Avoid re-authentication loops. Token-based sessions and trusted devices can help.

- Track drop-off metrics. Know where users quit. Then fix it.

Don’t just measure logins. Measure how many logins lead to meaningful action.

This Isn’t Just a UX Issue—It’s Strategic

In an age of open banking, embedded finance, and fintech partnerships, your login experience is a critical piece of your overall brand. A cumbersome login doesn’t just frustrate—it signals that your institution might not be as modern or agile as your competitors.

And when customers feel that friction every day?

They start looking for smoother paths elsewhere.

Final Thoughts: You’re Not the Customer Anymore

Here’s the hardest part for many banks to accept: the people designing the system aren’t the people using it.

Just because you’re comfortable navigating 2FA + PIN + grid card doesn’t mean your customers are.

We have to stop designing for the edge case, and start designing for the everyday case.

If your app makes checking a balance feel like defusing a bomb, it’s time to rethink your process.

Ready to Measure Your Friction?

The OptimizeCore® Scorecard assesses how your login flows measure up to customer expectations, compliance needs, and modernization goals. We help you spot bottlenecks before they become brand risks.

- Is your friction smart or arbitrary?

- Are your controls efficient or excessive?

- Do your flows encourage trust—or test patience?

Because your login is your first impression.

Let’s make sure it isn’t your last.

#CoreBankingTransformation #CoreBankingOptimization