In the AI era, no single vendor can do it all, winning banks build composable ecosystems they control, not dependencies they inherit.

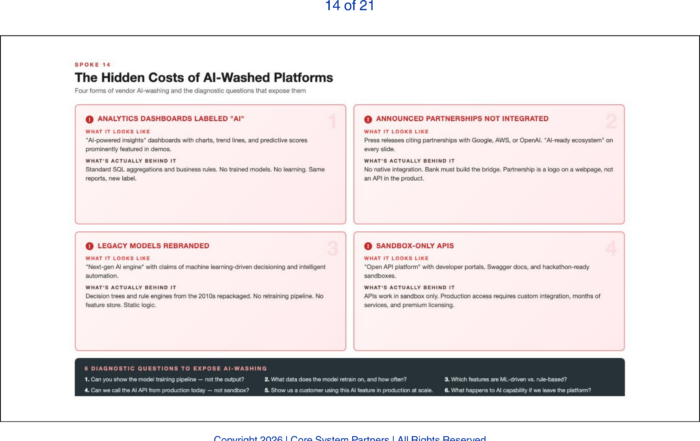

The previous two articles examined vendor selection and AI-washing, how to evaluate individual vendors and how to distinguish real capability from marketing. This article steps back to address the structural question: should a bank rely on a single vendor at all? The answer, in the AI era, is no.

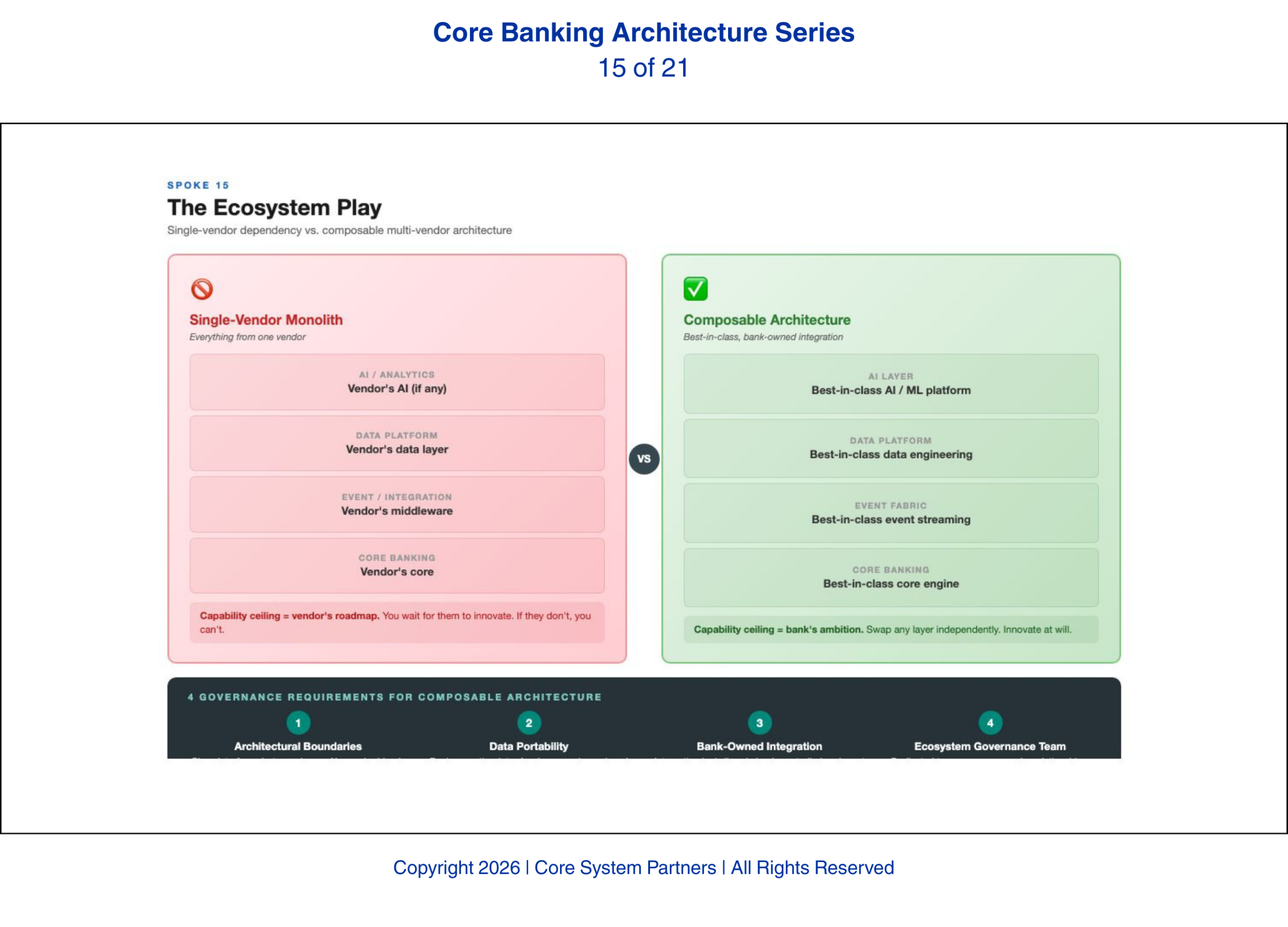

The single-vendor core banking model, one platform handles deposits, lending, payments, digital channels, data, and now AI, is fundamentally incompatible with AI-era banking. AI capability is evolving too fast and across too many dimensions for any single vendor to own the entire stack. The banks that will lead in AI are not looking for a single vendor with all the answers. They are building composable architectures: best-in-class components for each capability domain, orchestrated through a disciplined integration layer the bank controls.

This is not a license to collect vendors indiscriminately. Ungoverned vendor sprawl is as dangerous as single-vendor dependency. The ecosystem model requires governance that most banks have not yet built and the tension between ecosystem freedom and ecosystem discipline runs through every decision this article addresses.

Why Single-Vendor Fails in the AI Era

The argument for single-vendor platforms was always integration simplicity. One vendor means one data model, one API standard, one upgrade cycle, one support relationship. That simplicity came at a cost, the bank’s capability ceiling was set by the vendor’s roadmap, but the tradeoff was manageable when technology evolved at a pace vendors could match.

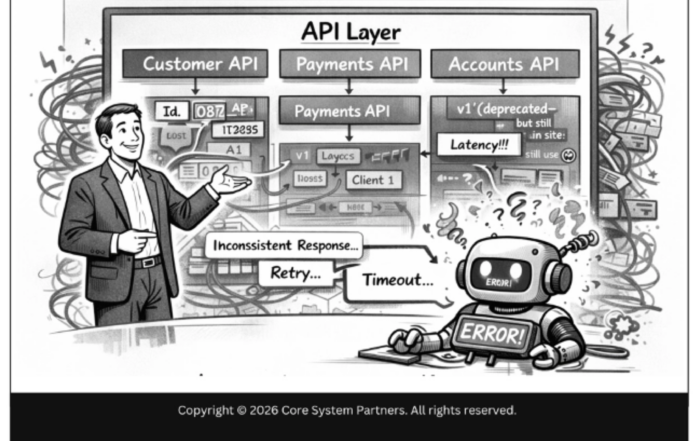

AI broke that equation. AI capability is advancing on multiple fronts simultaneously: large language models, computer vision, agent frameworks, orchestration engines, vector databases, embedding models, retrieval-augmented generation, and dozens of other capabilities that did not exist three years ago. No core banking vendor is leading in all of these areas. No core banking vendor is leading in most of them. The vendors that are leading, the AI-native companies, do not build core banking systems.

A bank that delegates its AI future to its core banking vendor is delegating it to a company whose primary expertise is transaction processing, not artificial intelligence. That company may build competent AI features over time. It will not build best-in-class AI capability. The gap between competent and best-in-class will widen every year as AI-native companies accelerate.

A bank that delegates its AI future to its core banking vendor is delegating it to a company whose primary expertise is transaction processing, not artificial intelligence.

The Composable Architecture

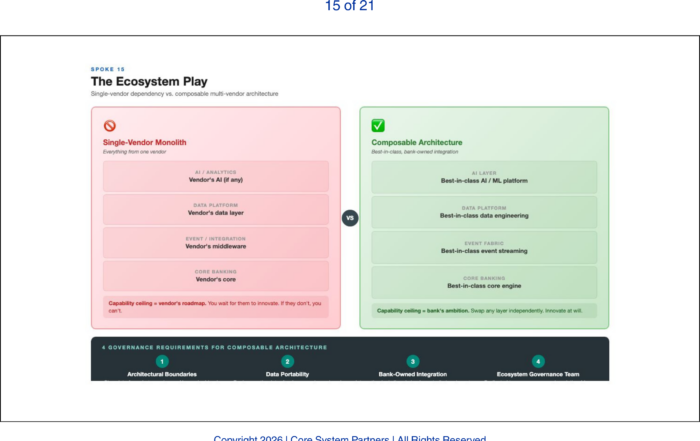

The alternative is composable architecture. The core banking platform handles what it does best: transaction processing, account management, and regulatory reporting. A separate data platform handles the data engineering that AI requires. A separate AI inference layer handles model deployment and orchestration. A separate event streaming platform provides the event fabric. Each component is best-in-class for its function, selected independently, and replaceable independently.

The mid-tier institutions we have worked with that are deploying AI fastest have already adopted this model. They run a core banking platform for systems of record, a cloud data platform for analytics and AI feature engineering, an AI orchestration layer for model management and agent deployment, and an event streaming platform for real-time event distribution. Each layer communicates through governed APIs and shared event schemas. No single vendor owns the stack. Community banks can pursue a simplified version of this model, fewer layers, more managed services, but the principle is the same: do not let a single vendor’s architecture constrain your AI ceiling.

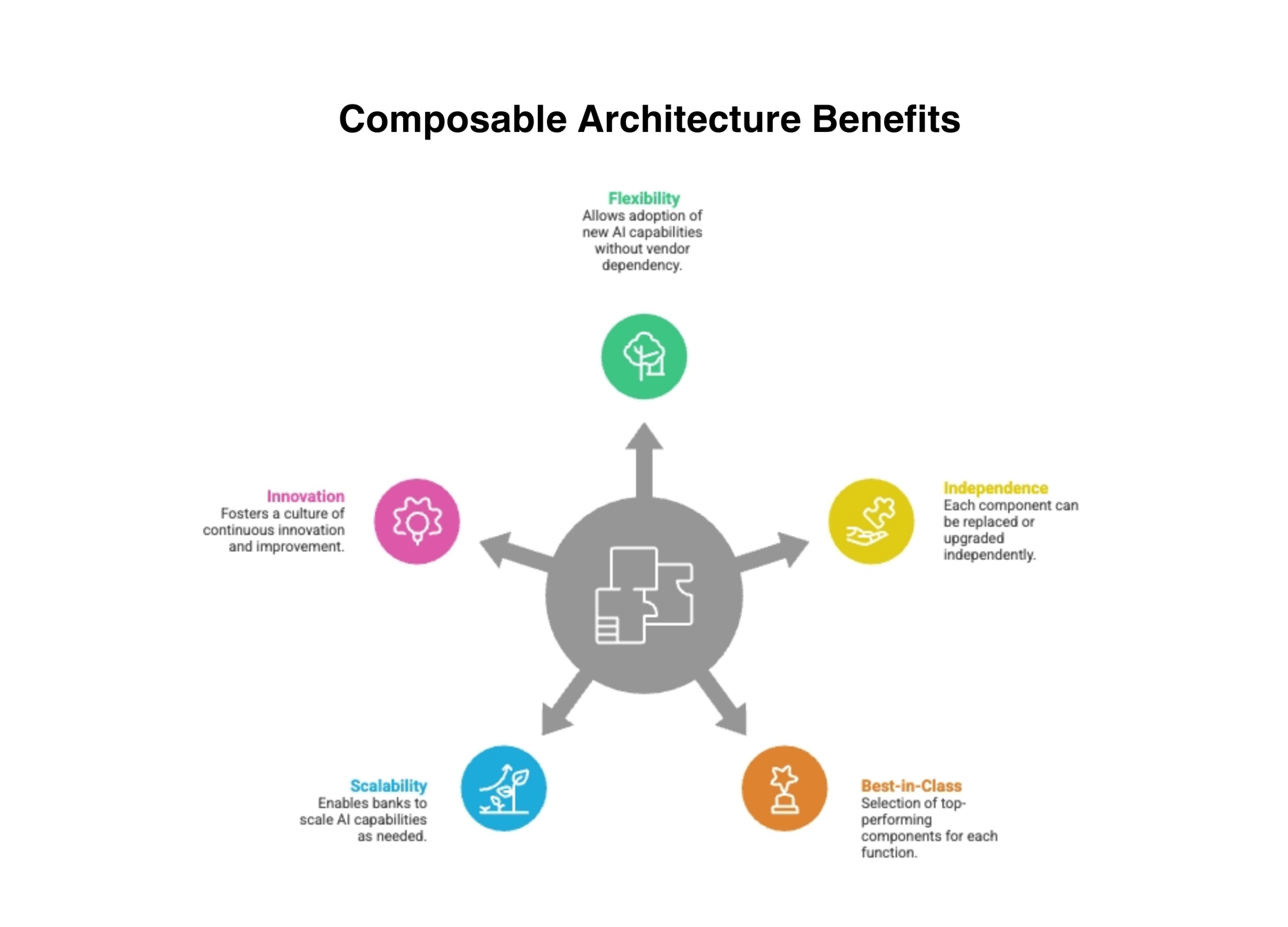

This architecture allows the bank to adopt new AI capabilities as they emerge without waiting for the core banking vendor to incorporate them. When a new model architecture proves superior for fraud detection, the bank deploys it in the AI layer without touching the core. When a better event streaming platform enters the market, the bank can migrate the event layer without disrupting the data platform. Each component evolves at its own pace. The discipline required to maintain this composability, rather than letting it collapse back into vendor dependency through convenience, is the governance challenge that follows.

Composable architecture gives banks the flexibility to innovate, scale and adopt AI, without vendor constraints.

The Governance Requirement

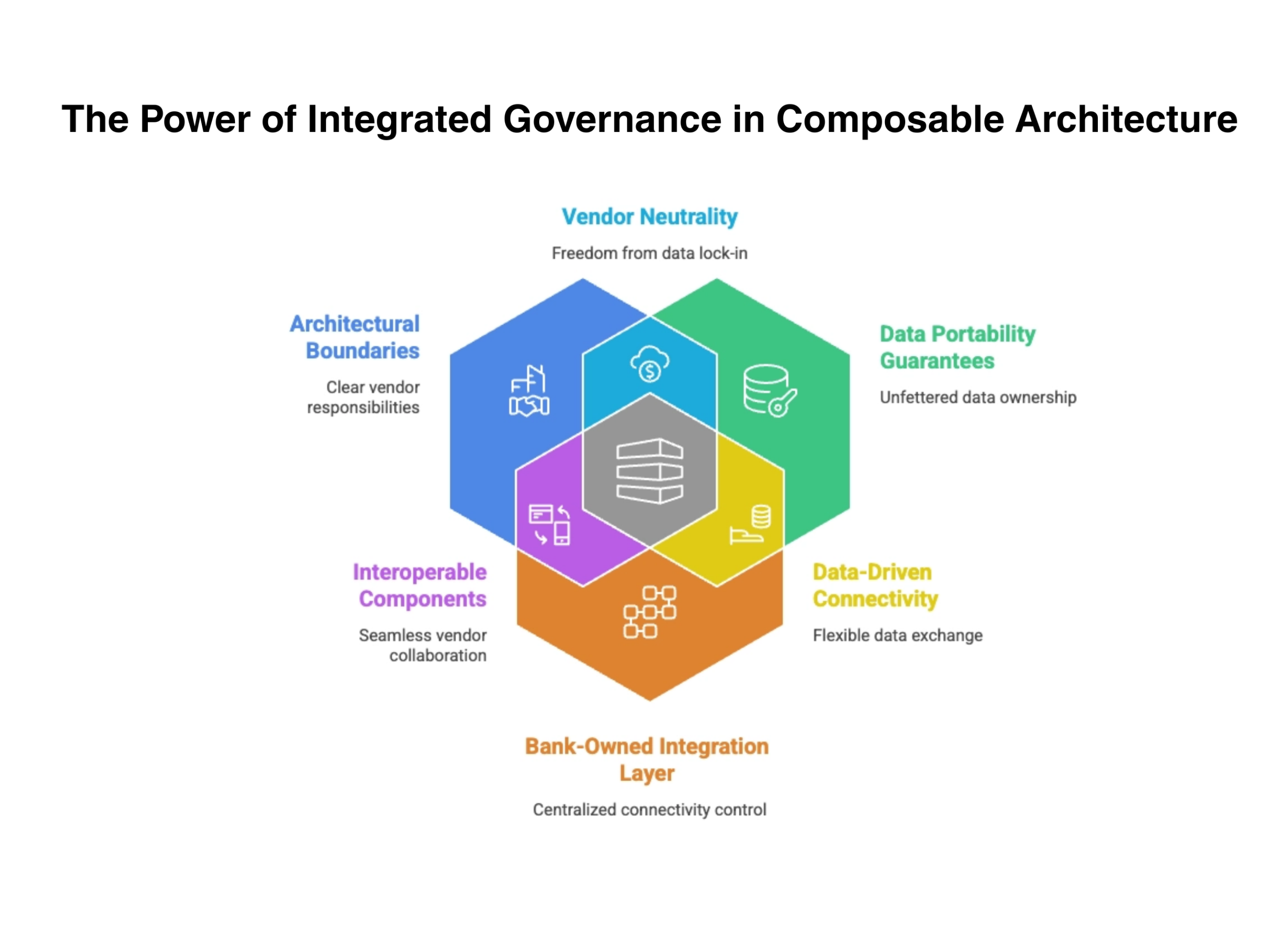

Composable architecture without governance is vendor sprawl. And vendor sprawl creates its own category of operational risk: conflicting data models across vendors, integration complexity that grows exponentially with each new component, contractual dependencies that limit the bank’s ability to change course, and operational support fragmentation where no single vendor owns the end-to-end outcome.

The first requirement is clear architectural boundaries for each vendor’s responsibility. The core handles transactions. The data platform handles analytics. The AI layer handles inference. No vendor’s scope creeps into another’s domain. When boundaries are unclear, vendors compete for the same territory and the bank pays for overlapping capability.

The second requirement is contractual data portability guarantees. No vendor can hold the bank’s data hostage. Every vendor contract must include explicit terms for data extraction in standard formats, at the bank’s discretion, without penalty. A bank that cannot move its data out of a vendor’s platform is not a customer. It is a captive.

The third requirement and the one most frequently overlooked, is a bank-owned integration layer. The middleware, the API gateway, the event routing must be controlled by the bank, not provided by a vendor. The risk of vendor-controlled integration is subtle and severe: the vendor that controls the integration layer controls the bank’s ability to swap any other component. It becomes the new single-vendor dependency, more deeply embedded than the core it was supposed to liberate the bank from. We have seen banks escape one vendor lock-in only to discover they had traded it for integration-layer lock-in that was harder to detect and more expensive to unwind. The bank must own the connective tissue of its architecture.

The fourth requirement is an ecosystem governance function. Someone in the bank, a team, not a committee, must be responsible for evaluating new components against the architectural standard, managing vendor relationships across the ecosystem, and ensuring that the composable architecture remains composable rather than devolving into another form of spaghetti.

Composable architecture works only with governance, without it, flexibility turns into fragmentation.

The Decision Window

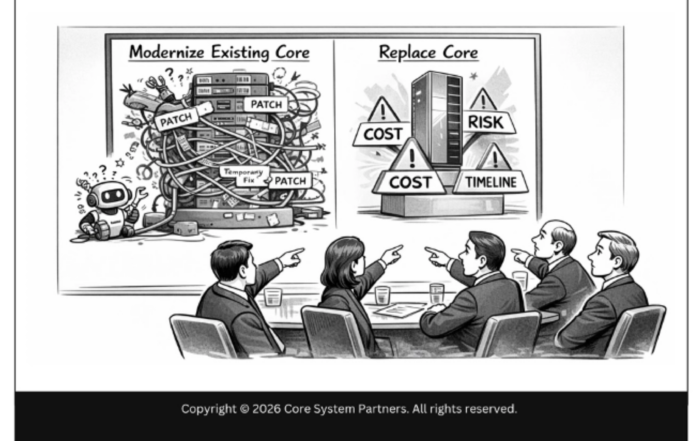

Banks that are still negotiating single-vendor all-in-one contracts in 2026 are making a decision that will take five years to undo. The contract itself may be seven to ten years. The architectural dependency it creates may last longer. The five years it takes to undo that contract is five years of AI capability foregone. Competitors will not wait.

The ecosystem model is not easy. It requires architectural discipline, governance investment, and operational maturity that many banks are still building. But the alternative , betting the bank’s AI future on a single vendor’s ability to keep pace with the fastest-moving technology category in history, is a bet that history is already proving wrong.

What Comes Next

Architecture, data, integration, governance, vendor strategy, the series has now addressed the technical and strategic foundations. But twenty-five years of watching bank transformations succeed and fail has taught us that the technical architecture is rarely what determines the outcome. The next section turns to the operating model: the organizational structures, governance cadences, and talent strategies that determine whether a bank can execute on the architecture it builds. Banks that get the architecture right but the operating model wrong end up with expensive infrastructure that nobody uses. The first of these articles examines why architecture governance itself must change , from a quarterly committee to a continuous operational capability.

Where to Start

If your bank is running a single-vendor stack and beginning to explore AI, or if you have already started accumulating AI vendors without a governance framework to manage them, the ecosystem question is already on your doorstep.

The CSP Transformation Readiness Scorecard evaluates your vendor ecosystem against the four governance requirements outlined in this article, architectural boundaries, data portability, integration layer ownership, and ecosystem governance maturity. It gives leadership teams a structured view of where ecosystem discipline exists and where vendor sprawl risk is building, in under an hour, with clear prioritization of where to act first.

If your AI strategy depends on a single vendor to deliver the majority of your AI capability, the governance requirements in this article are the ones you do not yet have and they are the ones that will determine whether the strategy executes.

If your institution is ready to move from awareness to action, visit coresystempartners.com/contact to start the conversation.

Next article in the series: The Architecture Operating Model Banks Must Adopt

Return to: Why AI makes modern core banking architecture non-negotiable

#CoreBankingTransformation #CoreBankingArchitecture