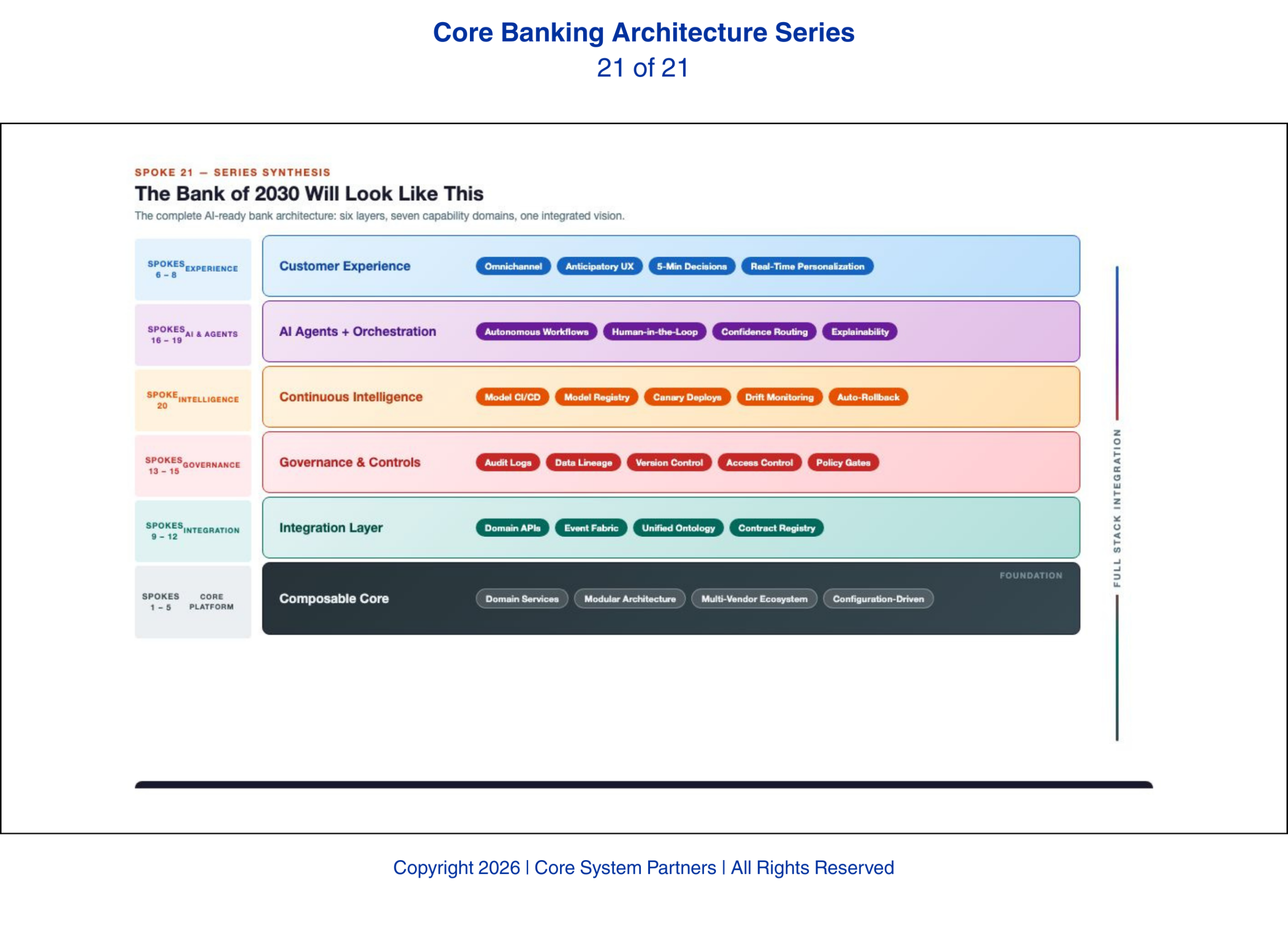

A six-layer blueprint of the AI-ready bank, illustrating how composable architecture, integration, governance, and AI agents come together to deliver real-time, intelligent banking experiences.

The bank of 2030 already exists in its foundations. What follows is what it looks like when fully assembled — a grounded projection from what the architectural leaders in banking are already building today. The technologies exist. The patterns are proven. The question is which banks will build it and which will not.

The Architecture

The 2030 bank runs a composable core with domain-separated services. Deposits, lending, payments, treasury, compliance, and customer management each operate as bounded domains with clean APIs, their own data stores, and their own event streams. The domains communicate through a unified event fabric that provides both real-time streaming and historical replay. Every domain publishes business events with semantic meaning — not database change logs — using a shared enterprise ontology.

That ontology is the bank’s semantic nervous system. Every system, every model, every agent speaks the same language. Customer means one thing. Account means one thing. Transaction means one thing. The ontology war that consumed the 2020s — where every system defined every entity differently — has been resolved through deliberate, persistent governance. The result is an enterprise where data flows seamlessly because every system agrees on what the data means.

The technology stack is not a single vendor’s product. It is an ecosystem of best-in-class components orchestrated through a bank-owned integration layer. The core handles transaction processing. A separate data platform handles analytics and feature engineering. An AI orchestration layer manages model deployment, agent coordination, and decision routing. An event streaming platform provides the fabric. Each component was selected for excellence in its domain and can be replaced independently when a better option emerges.

The Operations

AI agents handle the majority of routine decisions. Customer onboarding is agent-driven: identity verification, KYC screening, account opening, product assignment, and welcome communication all execute autonomously with human review only for exceptions that fall outside the agent’s trained parameters. Loan origination for standard products follows the same pattern — application intake, credit decisioning, document generation, and closing for straightforward applications are handled end-to-end by agents.

Humans focus on what humans do best: relationship management, complex credit structures, strategic advice, and the judgment calls that require experience, empathy, and contextual understanding that AI cannot replicate. A commercial banker in 2030 does not spend time on data entry, document chasing, or routine compliance checks. Those tasks are handled by agents. The banker spends time on the client relationship — understanding the business, structuring the deal, and providing counsel that creates genuine value.

Model operations is a standing discipline alongside technology operations. A dedicated team manages the CI/CD pipeline for models, monitors drift and performance, executes canary deployments, and manages rollbacks. Models are updated weekly or biweekly as new data improves their accuracy. The model registry tracks every version, every deployment, and every performance metric. The governance infrastructure captures every decision made by every agent and every model, stored in immutable audit logs accessible to risk, compliance, and examiners.

Architecture review is continuous, not episodic. The Architecture Review Board meets biweekly with cross-functional representation and genuine decision authority. Published architectural standards are enforced through automated compliance checks in the deployment pipeline. Architects are embedded in delivery teams, shaping designs as they emerge rather than reviewing them after the fact. Technical debt is visible, prioritized, and systematically retired.

The Customer Experience

The customer does not see the architecture. The customer sees the outcomes. Personalization is coherent across every channel because the data architecture is coherent underneath it. The mobile app, the website, the branch experience, and the call center all draw from the same unified customer view built on the enterprise ontology. A customer who starts a mortgage application on mobile, asks a question through the chatbot, and visits a branch to finalize has a seamless experience because every channel sees the same data, the same history, and the same context.

Decisions are faster and more accurate. A credit decision that took five days in 2024 takes five minutes in 2030 for standard applications. A fraud alert that took hours to investigate is resolved in seconds by an agent that has already correlated the transaction with the customer’s behavioral pattern, device history, and location data. The few cases that require human investigation arrive with a complete analysis package — the agent has already done the research and presented its findings for the analyst’s judgment.

Services anticipate needs rather than react to requests. The next-best-action engine — powered by real-time event streams from every domain — identifies customers approaching a financial transition and surfaces relevant products before the customer asks. A business owner whose receivables pattern suggests seasonal cash flow pressure receives a proactive line of credit offer. A depositor whose savings pattern suggests a major purchase is approaching receives investment optimization guidance. The bank is not waiting for the customer to call. The bank is calling the customer — through the right channel, at the right time, with the right offer.

The competitive consequence of this experience gap is self-reinforcing. A customer who receives a five-minute credit decision will not return to a bank that takes five days. A business owner who receives proactive cash flow guidance will not switch to a bank that waits for a phone call. The experience gap between AI-ready and legacy banks widens each year and becomes permanent — because the customers themselves will not tolerate going backward.

The Honest Truth

Every capability described above is the product of deliberate investment made years earlier. None of it arrives by default, and none of it can be compressed into a single-year catch-up sprint. The banks investing in this architecture now — modularizing their cores, building event fabrics, governing their data ontologies, disciplining their APIs, embedding governance in their infrastructure, building cross-functional operating models, and upskilling their people — are constructing the bank described above.

The banks that are not investing will face a choice. Some will be acquired by banks that did the work. Some will find a niche where the absence of AI capability does not matter — though that niche is shrinking every quarter. Some will attempt to catch up in 2028 or 2029 and discover that architectural foundations cannot be built in a year when competitors have been building for five.

The window for starting this work is not closing. It is narrowing. Every quarter of inaction is a quarter of compounding advantage for the banks that are moving.

The window for starting this work is not closing. It is narrowing. Every quarter of inaction is a quarter of compounding advantage for the banks that are moving.

The Next Step

This series has described what AI-ready banking architecture looks like, why it matters, and what it takes to build. The natural question is: where does my bank stand? The CSP Transformation Readiness Scorecard is designed to answer that question. It evaluates your bank’s current architecture against the standards described in this series — data ontology, API discipline, event capability, governance infrastructure, vendor architecture, operating model maturity, and talent readiness. The scorecard does not tell you what to buy. It tells you where you are, where the gaps are, and what to prioritize.

The architecture described in this series is achievable. It requires discipline, investment, and leadership. The banks that provide all three will build the future described here. The banks that provide none will become the future’s footnotes.

The 2030 bank described here is not a prediction. It is a blueprint being built right now, in institutions that made the architectural decisions three years ago that are paying off today.

If your institution is ready to move from awareness to action, visit coresystempartners.com/contact to start the conversation.

Next article in the series: Preparing For a World of Continuous Intelligence

Return to: Why AI makes modern core banking architecture non-negotiable

#CoreBankingTransformation #CoreBankingArchitecture